NRI company registration in India can feel complex multiple regulators, documentation requirements, and strict regulatory compliance. India today stands as one of the world’s fastest‑growing economies, offering a unique blend of tradition, innovation, and entrepreneurial energy. For Non‑Resident Indians (NRIs), this dynamic environment opens the door to limitless possibilities, from investing in its rapidly expanding economy and rising consumer base to building sustainable enterprises across diverse sectors. With initiatives like Make in India, Startup India, and Digital India, the business climate has become more transparent, investor‑friendly, and globally competitive.

NRIs can enjoy high returns, repatriate profits, benefit from tax incentives, and tap into India’s large market. Supportive business networks and industry hubs further ensure guidance and collaboration, making India a secure, attractive, and high‑potential destination for investment in India.

“India’s economic transformation is a testament to the resilience and ingenuity of its people.” Prime Minister Narendra Modi

Now is the perfect time for NRIs to explore India’s thriving opportunities, capitalize on its growth potential, and establish ventures that deliver both financial success and long‑term value. This guide preserves your original information while structuring it for search intent, readability, and conversions. For our experience and approach, see About Themis Law Associates.

Why Invest in India

India remains one of the fastest‑growing major economies, with national programs (digital infrastructure, manufacturing incentives, ease‑of‑doing‑business reforms) attracting the Indian diaspora. For NRIs, returning capital, skills, and networks is not only emotionally appealing but, under the right structures and compliance, financially attractive.

Central question: How can a Non‑Resident Indian establish and operate a compliant, tax‑efficient, scalable business in India today while legally repatriating profits and managing risks?

Executive Summary: What This Guide Contains

A quick snapshot of the steps, documents, timelines, and regulatory checkpoints for NRI company registration in India, so you know what to expect before you begin.

- Business entity selection for NRIs (pros/cons, formalities)

- How to start a company in India as an NRI: step‑by‑step operational roadmap

- Governing laws and regulatory authorities, you must know

- Capital/FDI routes and practical limits under FEMA

- Banking: NRE, NRO, FCNR, RFC; repatriation rules

- Taxation: corporate tax, TDS, capital gains, transfer pricing, DTAA

- Compliance obligations: GST, ROC filings, labour laws

- Practical risks and a compliance checklist

- Recent policy updates and next steps for first‑time entrepreneurs

Who this is for: First‑time NRIs and foreign nationals planning business setup in India who want clarity on documentation requirements, compliance timelines, and costs.

1) Choosing an Entity: Legal Forms Available to NRIs

Your legal form impacts tax treatment, compliance burden, investor acceptance, capital raising, and repatriation.

Private Limited Company (Pvt Ltd)

Why choose: Limited liability, credibility with banks/investors, easier to raise equity, and possible listing later.

Ownership by NRIs: NRIs/foreigners can hold 100% equity in many sectors under the FDI policy (subject to sectoral caps; automatic vs government route).

Regulatory touchpoints: MCA, RoC, Income Tax Department, GSTN (if applicable).

Key compliance: Annual filings (AOC‑4, MGT‑7), board minutes, statutory audit, periodic ROC fees.

Limited Liability Partnership (LLP)

Why choose: Lower compliance than Pvt Ltd in some areas; limited liability; tax transparency benefits for some structures.

For NRIs: NRIs can be partners; LLPs can receive foreign investment, but some restrictions may apply depending on business activity. Check sector‑specific FDI rules.

Key compliance: Annual Statement of Accounts & Solvency, income tax return, and LLP agreement governance.

Branch Office / Project Office (Foreign Company Routes)

Why choose: Entry for an overseas company without creating an Indian subsidiary; useful for market research, liaison, or executing specific projects.

Restrictions: Regulated by RBI and the Ministry of Commerce; activities are limited, and profit repatriation requires strict compliance and approvals.

Proprietorship & Partnership

Why choose: Simple structures for small firms.

Limitations: Unlimited liability; less attractive to outside investors.

Special Structures

Section 8 companies (non‑profit), trusts, and co‑operatives relevant for social or charitable enterprises.

Rule of thumb: For scale and external funding, a Private Limited Company is usually optimal; for low‑cost operations and partnerships, consider an LLP. If you are a foreign corporation looking for a presence without incorporation, evaluate branch/liaison options with RBI guidance. For entity selection and Companies Act guidance, consult our corporate lawyers in Hyderabad.

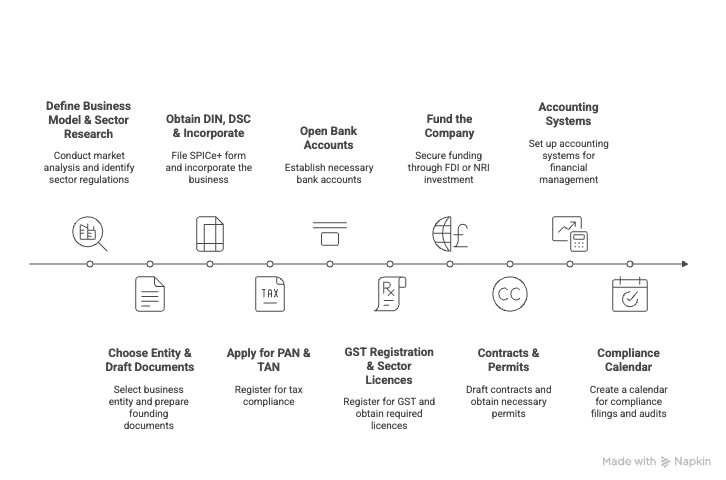

2) NRI Company Registration in India: Step‑by‑Step Roadmap

A pragmatic 10‑step roadmap (timelines assume documents are in order):

- Define business model & sector research (1–3 weeks): Market sizing, competitive analysis, sector regulators (some sectors require approval). Use Invest India’s “Setting Up Business in India” guide and sectoral sites.

- Choose entity & draft founding documents (1–2 weeks): MoA/AoA for companies; LLP Agreement for LLP.

- Obtain DIN, DSC & incorporate (2–4 weeks): File SPICe+ (INC‑32) with MCA. Working with an experienced Company Secretary in Hyderabad can streamline drafting and filings.

- Apply for PAN & TAN (2–3 weeks): Enable direct/withholding tax compliance.

- Open bank accounts: NRE/NRO/Business current account with an AD Category‑I bank experienced in NRI/FDI.

- GST registration & sector licences: Based on threshold/taxable supplies; add FSSAI/IEC/RBI etc. if applicable.

- Fund the company (FDI route/NRIs investment): Automatic vs government route; FEMA‑compliant inward remittances with KYC.

- Contracts & permits: Leases, vendor and employment contracts; local municipal permissions; labour law onboarding.

- Accounting systems: Bookkeeping, audit planning, professional tax, and monthly GST/ledger processes.

- Compliance calendar: Filings, audits, TDS/GST returns, and event‑based reporting.

Practical tip: Engage local legal/corporate counsel early to align entity selection, FEMA/FDI, banking, and repatriation plans.

3) Governing Laws & Primary Regulatory Authorities

Key laws:

- FEMA, 1999 foreign investment, remittances, repatriation (RBI enforcement)

- Companies Act, 2013, incorporation, governance, filings

- Income Tax Act, 1961, corporate/withholding tax, DTAA interface

- GST Act indirect tax via GSTN

- SEBI and sectoral acts (banking, insurance, telecom, defence, FSSAI, etc.)

Primary authorities: RBI, MCA/RoC, CBDT/Income Tax Dept., DPIIT/Invest India, GSTN, and sector regulators (SEBI, IRDAI, TRAI, FSSAI, etc.).

4) Capital & FDI: Routes, Caps, and Instruments

FDI routes:

- Automatic route: No prior government approval is required in many sectors.

- Government route: Sensitive sectors or higher equity thresholds require approval.

Sector caps: Vary by activity (e.g., insurance/defence/space have tiered caps). Always consult the latest DPIIT Consolidated FDI Policy.

Capital methods:

- Equity subscription (pricing/valuation as per FEMA)

- ECB/foreign loans within RBI norms

- Preference/convertible instruments are subject to guidelines

- Resident–NRI share transfers with valuation and tax checks

Repatriability: Equity sale proceeds are generally repatriable, subject to taxes and filings. From NRO, certain receipts are repatriable up to USD 1M per FY (with documentation); higher amounts need RBI approval.

5) Banking for NRIs: NRE, NRO, FCNR, RFC

Select accounts to optimise tax, repatriability, and currency risk.

NRE (Non‑Resident External) account

- Purpose: Park foreign earnings remitted to India

- Repatriability: Principal + interest fully repatriable

- Tax: Interest is typically tax‑exempt in India

- Use case: Operating funds with outward remittances

NRO (Non‑Resident Ordinary) account

- Purpose: Manage Indian‑sourced income (rent, dividends, sale proceeds)

- Repatriability: Up to USD 1,000,000 per FY (April–March), subject to taxes/documents; more needs RBI permission, see the RBI’s FAQs on non‑resident accounts

- Tax: Interest taxable; TDS applies

FCNR (B) deposits

- Purpose: Term deposits in foreign currency

- Tax: Interest is generally exempt in India

RFC (Resident Foreign Currency) account

- Purpose: For returning NRIs to retain foreign currency holdings

Set‑up advice: Maintain NRE/FCNR (for foreign revenue) and NRO (for Indian revenue). Keep clear audit trails; AD banks will verify the source of funds for large remittances.

6) Taxation Essentials for NRI‑Owned Businesses

Residency & scope: NRIs are generally taxed on India‑sourced income; residents on global income (as per stay‑based tests).

Major tax heads:

- Business income (profits), corporate/partnership rules

- Dividend income taxable with TDS (DDT abolished; dividends taxed to shareholders)

- Capital gains depend on the asset/holding period

- Interest income NRE/FCNR is often exempt; NRO interest is taxable

- Withholding (TDS) on payments to non‑residents (interest, royalties, FTS, dividends)

DTAA: Relief via TRC + Form 10F and declarations. Plan treaty benefits and foreign tax credits.

Repatriation & tax: Repatriation itself isn’t a separate tax event, but banks check tax clearance and may require Form 15CA/15CB.

Typical flow: Invest → earn profits → pay corporate tax → distribute dividends (TDS) → repatriate net cash as per FEMA/RBI.

7) Compliance Calendar & Event‑Based Filings

Recurring:

- ROC filings (Companies): AOC‑4 (financials), MGT‑7 (annual return)

- Income tax: ITR (e.g., ITR‑6 for companies), quarterly TDS deposits/returns

- GST returns: Monthly/quarterly and annual, as applicable

- Statutory audit (threshold‑based)

- Transfer pricing documentation (master/local files when thresholds are met)

- Foreign investment reporting: FLA return; RBI filings via AD bank

Event‑based: FEMA/AD filings for inward remittances and equity subscriptions; Form 15CA/15CB for remittances; RBI permissions for repatriation > USD 1M; labour/employment registrations (PF/ESI, professional tax).

Operational checklist: Monthly bank reconciliation, GST bookkeeping, TDS with Form 26AS match, annual statutory audit, and on‑time ROC.

8) Repatriation in Practice: Bringing Profits Home

- Ensure tax compliance (corporate tax paid; dividend/interest TDS deposited)

- Obtain CA certificate (Form 15CB) and file Form 15CA/15CB official process guide (as required)

- Use the right accounts: NRO for India‑sourced funds under the USD 1M cap; NRE/FCNR are typically simpler to repatriate

- AD bank processing: Bank verifies documents and tax status before outward remittance

- DTAA/FTC: Claim relief in the resident country using TRC and Indian tax proofs

Example: Repatriating property sale proceeds uses the NRO route with CA certification and adherence to the USD 1M limit unless RBI permission is obtained.

9) Financing, Cost & Expected Returns (Illustrative)

- Equity vs debt: Equity avoids fixed servicing; debt (including ECBs) creates deductible interest but has RBI/BEPS constraints

- Illustrative micro‑manufacturing unit:

- Setup capex: ₹1.5–₹5 crore (machinery, fit‑out)

- Working capital: 25–50% of annual COGS

- Year 1–3 revenue: 0.5–2× initial investment (sector‑dependent)

- EBITDA: Manufacturing 8–20%; services often higher

- Repatriation (net): After corporate tax and dividend TDS; actual outcome depends on DTAA and resident‑country rules

Note: Always run numbers with your accountant for precise forecasts.

10) Recent Policy Changes (2023–2025 Highlights)

- FDI liberalisations: Higher automatic route access in select sub‑sectors (insurance/defence/space/telecom)

- RBI reiteration: USD 1M NRO repatriation limit (documentation + CA certs)

- Tax admin updates: ITR deadlines/procedures evolve annually; monitor CBDT circulars

Impact: Easier inbound investment in select sectors; compliance remains detailed.

11) Risk Management & Mitigation

Common risks: Currency volatility, regulatory change, transfer pricing disputes, and operational partner risk.

Mitigation: Strong local counsel/CA/CS, staged JV investments, dual reporting (IFRS/Ind AS) for cross‑border stakeholders, and appropriate insurance.

12) Practical Checklists & Templates (Before You Invest)

Documents to prepare: Passport, overseas address proof, PAN (apply if needed), TRC for DTAA, source‑of‑funds documentation, board/shareholder approvals, CA valuation report (where needed).

On incorporation day: DSCs for directors, DINs, MoA/AoA finalised, registered office proof, ID/address proofs.

For repatriation: Filed returns, tax payment receipts, Form 15CB, bank declarations.

13) Recommendations & Next Steps (Action Plan)

A prioritized checklist to move from decision to NRI company registration in India through banking, FEMA/FDI filings, and annual compliance, so you know exactly what to do next.

- Pre‑investment legal & tax due diligence (FEMA/FDI route check; sector approvals)

- Open NRE & NRO with an experienced AD bank; set up the company’s current account

- Align investment instruments (equity vs convertible) with exit plans

- File RBI/FEMA returns (FLA, share allotment reporting) on time

- Engage CA and CS for annual compliance, transfer pricing, Form 15CA/CB

- Monitor DTAA & tax changes in India and your resident country

FAQs for First‑Time NRI Business in India

How long does NRI company registration in India take?

Typically, 3–6 weeks for incorporation if documents are complete; licensing and banking can add time.

Can I own 100%?

In many sectors under the automatic route, yes (subject to sector caps/conditions).

How soon can I repatriate profits?

After taxes/compliance are cleared, the NRO route allows up to USD 1M per FY for eligible receipts.

How we help you in NRI Company Registration

A quick look at the real hurdles first‑time NRI founders face and how our team addresses each with clear processes, firm compliance timelines, and transparent costs.

- Regulatory complexity: We translate multi‑agency rules (RBI, MCA, GSTN, DPIIT) into an actionable timeline

- Documentation requirements: We prepare/review KYC, SPICe+, PAN/TAN, GST, FEMA/AD filings, and Form 15CA/CB

- Compliance timelines: We set up an annual calendar (ROC, GST, TDS, FLA) with reminders

- Cost clarity: We scope incorporation, licences, and annual compliance to avoid surprises

- Legal uncertainty: We provide written opinions on FDI route/sector caps and repatriation

Conclusion

Establishing and operating a business in India as an NRI is highly feasible and attractive, provided your business setup is aligned with FEMA/FDI, tax, banking, and reporting rules. If you’re a first‑time entrepreneur worried about paperwork, compliance timelines, or hidden costs, you don’t have to figure it out alone.

Contact our Hyderabad team for a 20‑minute consultation. We’ll map your entity choice, bank accounts, filings, and repatriation plan so you can focus on growth while we manage the regulatory compliance.